Credit Ratings and Their Impacts on the Real World

As part of our case studies, we will take a look and explain what are credit ratings and the impacts they have on companies. This is quite important nowadays that companies are in a tougher market environment than in previous years. Why are companies in a tougher market environment? Well, the global economy is in an environment where interest rates are increasing. This is impacting companies, specifically the companies that have significant amounts of debt. Therefore, understanding credit ratings is crucial for businesses to navigate such conditions. Let's start with the basics.

Who Performs the Credit Ratings?

Credit ratings are typically performed by specialized credit rating agencies such as S&P Global, Moody's, and Fitch Ratings. These agencies assess the creditworthiness of companies, governments, and other entities that issue debt securities such as bonds.

These agencies use a standardized system of rating that evaluates various factors such as financial performance, market conditions, and management strategies to determine the creditworthiness of the issuer. The resulting credit rating is expressed as a letter grade or score that indicates the level of risk associated with the issuer's ability to repay its debts.

What is a Credit Rating?

A credit rating is simply a score representing how trustworthy a company is when it comes to paying the principal amount and interest on debt issued. A good credit rating will give a company easy access to debt at a relatively cheap price. On the other hand, a bad credit rating will make it difficult for a company to access debt markets, additionally, it will make it expensive for a company to borrow money, meaning the interest paid on debt will be higher.

Credit rating scores:

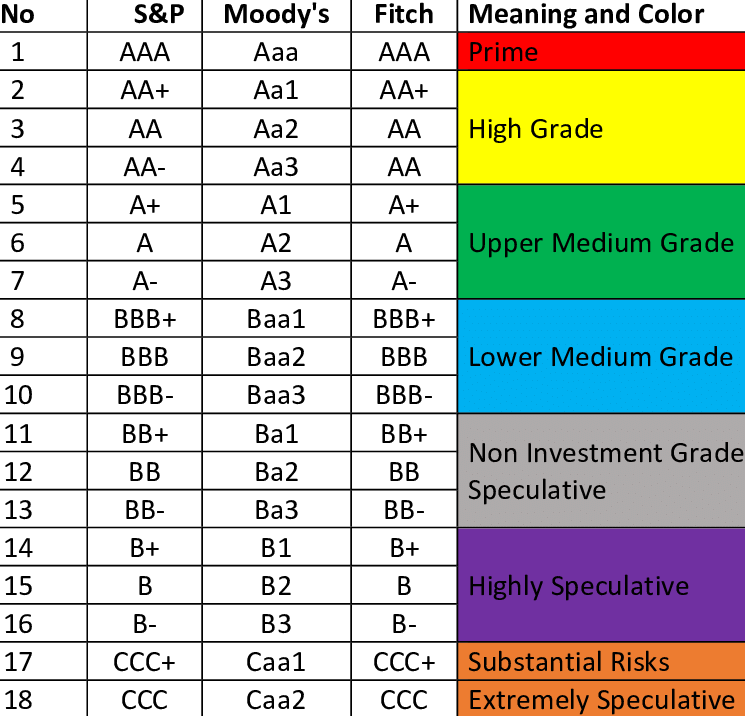

Credit scores usually range from AAA+ (Prime / Best rating) to CCC or lower (Extremely Speculative / Worst rating). Ratings that are below BBB- are considered sub-investment grade which makes it more difficult for companies to find debt funding opportunities as many institutional investors are not allowed to invest in them or need many more approvals to invest in sub-investment grade debt. A good credit rating (Above Investment Grade) will give a company easy access to debt and relatively cheap funding opportunities. Essentially a lower credit rating translates into a lower appetite for the company's debt as well as higher rates to be paid for debt issued.

Credit Rating Scores by the Different Rating Agencies:

Probability of Default Based on Credit Rating:

What are the Impacts Credit Ratings have on Companies?

Rating agencies assign credit ratings to companies based on their financial performance, market conditions, management strategies, etc. The credit rating of a company tells investors what the probability of default on its debt is. As it can be seen from the table above a higher credit rating means a lower probability of default while a lower credit rating means a higher probability of default.

Again, it is important to note that institutional investors have more restrictions when it comes to investing in debt that is below investment grade (Below: BBB-), so the debt market is considerably smaller for below-investment-grade companies. As the debt market for below-investment-grade debt is smaller it means there is less demand, to create demand companies need to offer higher interest rates on the debt they issue. As a result, companies with lower credit ratings pay higher interest rates.

Examples of Companies with Different Credit Ratings:

Let’s take the above companies and their credit ratings as references and let’s look at the impacts these ratings have on them.

Taking the above-mentioned companies and their respective credit ratings into account, let us examine the impacts of these ratings on their financing. It is evident that Berkshire Hathaway and Apple are assigned the highest credit ratings. This implies that both corporations will encounter little resistance to accessing debt capital markets whenever they desire to issue new debt or refinance existing debt. The outstanding credit rating of these entities ensures substantial demand for their bonds.

While Kraft Heinz and Heineken have credit ratings that are not as high as Berkshire Hathaway or Apple, they are still deemed to be investment-grade companies. Their credit ratings surpass the minimum threshold of BBB- or Baa3. These two corporations will have no trouble obtaining funding in case they need to issue new debt or refinance existing debt. However, they will have to pay higher interest rates than Berkshire Hathaway or Apple to compensate for the slightly elevated risk of default.

Lastly, Rolls Royce has the weakest credit rating among the five companies, and it is classified as a sub-investment grade. Consequently, if Rolls Royce plans to issue new debt or refinance existing debt, it will face more difficulty in attracting potential investors, and the investors who do agree to lend to Rolls Royce will demand a higher interest rate as compensation for the increased risk of default.

We are leaving an example of what rating agencies write for investors when discussing their rating decisions on companies. For this, we have taken the example of Heineken.

Link: sp-reseach-update-heineken-nv-update-31mar2022.pdf (theheinekencompany.com)

Factors Impacting Credit Ratings of Companies:

Evidence shows that credit ratings are primarily related to two financial indicators: i) size in terms of sales or market capitalization and ii) interest coverage in terms of EBITDA.

o EBITDA: Earnings before Interest, Taxes, Depreciation, and Amortization.

Size: Size is one of the important factors when it comes to a company’s rating. Either by market capitalization or by revenues per year. It is important to note that most if not all companies with a AAA rating have a market capitalization higher than $50 billion.

o Market Capitalization: Number of share outstanding multiplied by price per share.

You may be asking yourself why size is so important. Well, larger companies usually have more than one revenue stream, meaning they are diversified. In essence, big companies have many different revenue streams offsetting each other. So, if one revenue stream receives a shock the other streams will be able to keep generating money.

Interest coverage: This is the most relevant and is a straightforward indicator of a company’s ability to service its debt obligations.

o Interest Coverage: EBITDA or Cash Flow from Operations / Interest

Interest Coverage differs by industry and company. For example, telecommunications companies have a better credit rating than other industries at the same level of interest coverage. This is because industries and companies with more EBITDA or Cash Flow from Operations volatility need higher interest coverage ratios to attain a given credit rating.

o More volatility means there is higher risk that the company will not have sufficient cash flow to pay for its debt obligations in the future.

Conclusion about Credit Ratings and Their Impacts:

Credit Ratings help investors and lenders to assess the creditworthiness of a company, which is important when deciding whether to invest in or lend money to the company. The credit rating provides an independent and unbiased assessment of the risk of default or bankruptcy.

Credit ratings can affect the cost of borrowing for a company. If a company has a high credit rating, it can borrow money at a lower interest rate than a company with a lower credit rating. This can result in significant savings for the company over time.

Credit ratings can also affect the company's ability to borrow money. A low credit rating may make it difficult for a company to obtain financing, as lenders may be reluctant to lend money to a company with a higher risk of default.

Credit ratings can impact the company's reputation. A high credit rating can enhance a company's reputation and increase its credibility with customers, suppliers, and other stakeholders.